Futures Education Center

Watch how to execute the spread

Enter the mind of a trader as they trade the soybean crush spread, with every decision and step explained using TradeStation tools.

Watch nowWatch Webinar

The soybean crush spread captures the processing margin between raw soybeans and their refined products, soybean meal and soybean oil, offering traders a way to participate in grain market dynamics with potentially lower volatility and more defined risk than outright futures positions.

Watch webinarUnderstanding the Soybean Crush Spread: A Comprehensive Guide to Grain Futures Spreads

The grain futures markets offer sophisticated traders—and those learning advanced spread techniques—unique opportunities to capture processing margins between raw agricultural commodities and their refined products. Among these opportunities, the soybean crush spread is one of the most actively traded grain spread strategies in the futures markets.

The crush spread reflects the economics of crushing soybeans into soybean meal and soybean oil, creating a trading strategy that can potentially profit from changes in this processing relationship regardless of the absolute price direction of soybeans. This article will explore how the crush spread works, why traders implement these spread strategies, and the critical risk management considerations you need to understand before trading.

We'll also examine how TradeStation's FuturesPlus platform provides comprehensive tools for analyzing, executing, and monitoring these complex multi-leg trades, along with guidance on using simulated trading to practice before risking real capital.

What is the soybean crush spread?

The soybean crush spread represents the processing margin earned in converting soybeans into their end products. When processors crush soybeans, they produce two primary products: soybean meal, used mainly for animal feed, and soybean oil, used in cooking oils, biodiesel, and industrial applications. The crush spread expresses this processing relationship through three distinct futures contracts traded on the Chicago Board of Trade (CBOT):

Soybeans (ZS) – The raw commodity

Soybean Meal (ZM) – The first derived product used for livestock feed

Soybean Oil (ZL) – The second derived product used in food and industrial applications

Long crush vs. short crush

There are two fundamental ways to trade the crush spread, each designed to potentially profit from distinct market conditions:

Long crush (reverse crush): This strategy involves buying soybean meal and soybean oil futures while selling soybean futures. A long crush position looks to profit when the processing margin expands, meaning the combined value of meal and oil rises relative to the cost of raw soybeans. Traders might implement this strategy when they believe crushing margins are too narrow and likely to widen due to strong demand for meal or oil, weak soybean prices, or seasonal patterns favoring wider margins.

Short crush (traditional crush): This strategy involves buying soybean futures while selling soybean meal and soybean oil futures. A short crush position profits when processing margins narrow, which occurs when soybeans become more valuable relative to their processed products. This can happen during periods of strong export demand for whole soybeans, when demand for meal and oil weakens, or when supply constraints affect the finished products more than raw soybeans.

Together, these two approaches allow traders to position around whether crushing margins will widen or narrow.

The board crush: proper contract weighting

While some traders use a simplified one-to-one-to-one approach (buying or selling one contract each of soybeans, soybean meal, and soybean oil), this equal weighting doesn't accurately reflect the real-world processing relationship. Each contract represents different quantities, and the actual crushing of soybeans yields specific proportions of meal and oil.

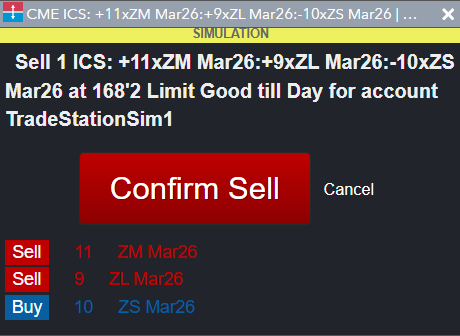

The exchange created what's called the board crush to address this issue. The board crush is a properly weighted structure comprising 30 contracts:

• 10 Soybean futures contracts

• 11 Soybean Meal futures contracts

• 9 Soybean Oil futures contracts

This 10:11:9 ratio more accurately reflects the relationship among these products and is the industry standard for professional crush spread trading. It accounts for differences in contract sizes and typical yield ratios, making it a more realistic structure than equal weighting.

Benefits of Trading the Crush Spread

Spread trading offers several compelling advantages over taking outright directional positions in individual futures contracts. Understanding these benefits can help you determine whether crush spread trading aligns with your trading objectives and risk tolerance.

Reduced margin requirements

Exchanges recognize that spread positions involve offsetting risk across related contracts. When you're long one leg and short another, your directional exposure is limited to the relationship between the products rather than their absolute price movements. As a result, exchanges typically require significantly lower initial and maintenance margins for spread positions than for outright futures positions.

This capital efficiency allows traders to deploy their capital more effectively across multiple opportunities or to maintain larger positions with the same capital base. However, it's critical to understand that reduced margins do not mean reduced risk. Lower margin requirements can tempt traders to over-leverage their positions, a topic we'll discuss in detail in the risk management section.

Lower volatility profile

Spread positions generally exhibit lower volatility than outright positions because you're trading the relationship between related commodities rather than their absolute price direction. While soybean prices might swing dramatically on weather reports, crop estimates, or export announcements, the processing margin (the crush spread) tends to be more stable.

For example, if a drought forecast pushes soybean prices sharply higher, soybean meal and soybean oil prices typically rise as well, since they're derived from soybeans. The crush spread focuses on how these products move relative to soybeans, rather than their absolute price levels. This relative stability can make spread positions more predictable and easier to manage than outright positions.

Focus on processing economics

The crush spread lets you trade the economics of soybean processing without taking a directional view on soybean prices. You can profit from your analysis of supply and demand factors affecting crushing capacity, meal demand from livestock producers, or oil demand from biodiesel manufacturers, regardless of whether soybeans themselves rise or fall.

This fundamental focus can be especially appealing to traders with expertise in agricultural markets, processing economics, or specific end-use industries. For instance, if you understand livestock feeding patterns and anticipate strong meal demand during certain seasons, you can structure crush spread trades to profit from that knowledge while avoiding exposure to general grain market volatility.

Reports like this one from USDA.gov can help with fundamental analysis of crush spreads.

More defined risk parameters

Relationships among soybeans, meal, and oil tend to trade within historical ranges. While these ranges can expand or contract, they offer more defined risk parameters than outright positions, where price movement is theoretically unlimited. Traders can analyze historical spread values to identify extreme readings and develop mean-reversion strategies based on the spread returning to more typical levels.

However, it's essential to note that historical relationships can and do break down. External shocks, fundamental shifts in supply or demand, or regulatory changes can push spreads beyond historical ranges and keep them there for extended periods. Past patterns provide context but never guarantee future behavior.

Understanding correlation risks and margin considerations

While spread trading offers lower volatility than outright positions, it's critical to understand that spreads carry their own unique risks. Chief among these is correlation risk and the margin complexities that can arise during periods of market stress.

Correlation risk: When relationships break down

The three contracts in a crush spread don't always move in perfect lockstep. Correlation risk is the possibility that the historical relationship between the legs of your spread may break down, causing unexpected losses even though you're theoretically hedged.

Several factors can disrupt typical correlations:

Divergent demand patterns: A surge in biodiesel production might push soybean oil prices higher, independent of meal prices. Conversely, an outbreak of livestock disease might devastate meal demand while oil demand remains strong, causing the spread to deviate from historical patterns.

Export policy changes: Government policies might favor exports of whole soybeans over processed products, or vice versa. Trade restrictions or tariff changes can create artificial price distortions that disproportionately affect one product over others.

Processing capacity constraints: If crushing facilities are constrained by maintenance, weather events, or other factors, this can disrupt the normal supply relationship between raw soybeans and their processed products.

Seasonal factors: Agricultural markets experience pronounced seasonal patterns. Planting season, growing conditions, harvest timing, and seasonal demand shifts can all affect how these products relate to one another at different times of the year.

When correlations break down, spread positions can experience significant losses. You might enter a long crush expecting margins to widen based on typical seasonal patterns, but find yourself facing losses if meal demand collapses while oil prices remain flat, or if unexpected export demand for whole soybeans drives soybean prices higher while product prices lag.

Margin Complexities

While initial margins for spreads are typically lower than outright positions, margin considerations are more complex than they might first appear:

Initial vs. maintenance margins: You need to maintain adequate capital reserves not just for initial margins, but for potential maintenance margin calls during adverse price moves. If the spread moves against you, you may receive margin calls requiring immediate capital injection to maintain your position.

Per-leg margin calculations: Each leg of the spread requires separate margin calculations. While the exchange offers reduced margins for the overall spread position, individual legs still carry their own margin requirements. During periods of extreme volatility, exchanges may increase margin requirements across all positions, potentially affecting your capital requirements mid-trade.

Mark-to-market risk: Futures positions are marked to market daily, meaning gains and losses are realized daily through your margin account. A series of adverse daily settlements can quickly deplete your margin cushion, even if your long-term thesis remains intact.

Volatility-driven margin increases: During periods of market turbulence, exchanges can increase margin requirements on short notice. This means you could face higher capital requirements mid-trade, regardless of your position's current profit or loss.

Together, these factors mean margin management is just as critical as trade selection in spread trading.

Leverage and Position Sizing: Managing Capital Wisely

The reduced margin requirements in spread trading create both opportunities and risks through leverage. Understanding how to size positions appropriately is one of the most critical skills for successful spread trading.

The Overleveraging Trap

One of the most common mistakes in spread trading is overleveraging. Just because you can take a larger position with less capital doesn't mean you should. While a single crush spread might require only a fraction of the margin of an outright soybean position, the temptation to "size up" because margins are low can expose you to unacceptable risk.

The psychological trap is subtle yet dangerous: traders see the low margin requirements and think, "I can control a much larger position with the same capital." This logic overlooks the fact that, while margins are lower, the potential for loss remains very real. A spread moving against you can generate significant losses, and those losses are magnified if you've increased your position size to match the reduced margin requirements.

Proper Position Sizing Framework

Effective position sizing for crush spreads should account for multiple factors:

Total account size and risk capital: Determine what percentage of your total trading capital you're willing to allocate to commodity spreads. This should be a percentage you can afford to lose without jeopardizing your overall financial stability. Many professional traders limit commodity exposure to a fraction of their total portfolio.

Per-trade risk limits: Set the maximum dollar amount you're willing to risk on a single trade. A common guideline is to risk no more than 1-2% of account equity per position. For a $100,000 account, that means risking no more than $1,000-$2,000 on a single crush spread trade.

Historical spread volatility: Analyze the typical daily or weekly volatility range of the specific spread you're trading. Understanding how much the spread typically moves helps you size your position to stay within your risk tolerance. If a spread moves $500 per day on average and you can only afford to lose $1,000, your position size must account for potential adverse moves over multiple days.

Stop-loss distance and tick value: Calculate the dollar value per tick for your spread, then multiply by your planned stop-loss distance. If your stop is 50 ticks away and each tick represents $10 in P&L, your maximum risk per spread is $500. Adjust your position size so this dollar risk matches your per-trade risk limit.

Portfolio correlation: Consider how your crush spread position correlates with other positions in your portfolio. If you're already long in grain markets through other vehicles, adding a long crush position may concentrate your risk beyond your per-trade risk limits. Diversification across spread types, markets, and asset classes helps manage overall portfolio risk.

Remember: trading a spread rather than an outright position doesn't change the fundamental principle that each trade should risk only a small, predetermined percentage of your total capital. Discipline in position sizing separates professional traders from those who blow up their accounts.

Entry, exit, and stop placement strategies

Developing a systematic approach to entries, exits, and stops is crucial for crush spread trading. Without clear criteria for when to enter, take profits, and cut losses, traders often make emotional decisions that undermine their long-term profitability.

Watch how to execute the spread

Enter the mind of a trader as they trade the soybean crush spread, with every decision and step explained using TradeStation tools.

Identifying entry points

Effective entry strategies for crush spreads often rely on a combination of technical, fundamental, and seasonal analysis:

Historical seasonal patterns: Crushing margins tend to follow seasonal patterns tied to harvest timing, livestock feeding cycles, and biodiesel production. For example, crush margins typically narrow during harvest when soybean supply is abundant, or widen in spring when livestock feeding demand for meal rises. While seasonal patterns don't guarantee future performance, they provide a framework for understanding typical spread behavior.

Technical analysis of the spread: Traders can apply technical analysis directly to the spread value itself, identifying support and resistance levels, moving average crossovers, momentum indicators, or chart patterns. For instance, if the crush spread consistently bounces off a specific support level, that might represent a low-risk entry point for a long crush position.

Fundamental supply/demand analysis: Understanding the fundamental factors affecting crushing economics can inform entry timing. This might include analyzing crushing capacity utilization, export demand for meal and oil, biodiesel production forecasts, livestock feeding patterns, or soybean supply estimates. If fundamentals suggest crushing margins should widen, but the spread is currently narrow, that might represent a buying opportunity.

Mean reversion strategies: When the crush spread deviates significantly from historical norms or expected fair value, traders might implement mean reversion strategies, expecting the spread to eventually return to more typical levels. This approach requires careful analysis of whether the deviation represents a temporary anomaly or a fundamental shift in market structure.

Planning your exit strategy

Exit strategies should be defined before entering the trade. Knowing your exit criteria in advance helps remove emotion from the decision-making process:

Profit targets: Set specific profit targets based on historical spread ranges or technical resistance/support levels. If the crush spread typically trades between -$20 and $40, and you enter a long position at -$10, you might target an exit at $30, which represents a move toward the upper end of the historical range.

Time-based exits: If the spread fails to move as expected within a specific timeframe, consider exiting even if you haven't hit your profit target or stop loss. This approach recognizes that capital tied up in non-performing positions has an opportunity cost. For example, if your thesis is based on seasonal factors that should play out within 30 days, and nothing happens in that timeframe, the trade might no longer be valid.

Fundamental exits: If the underlying thesis for your trade changes, consider exiting regardless of current profit or loss. For instance, if you entered a long crush expecting strong meal demand, but news breaks of a major livestock disease outbreak that will devastate that demand, exit immediately, even if you haven't hit your stop-loss yet.

Trailing stops: As the spread moves in your favor, consider using trailing stops to protect profits while allowing the position to continue working if the move persists. This technique helps you capture larger moves while protecting against sudden reversals.

Stop-loss placement for spread positions

Stop-loss placement for spreads requires different thinking than stops for outright positions. Because you're managing three separate contracts, you need to focus on the spread value itself, not just the individual legs:

Dollar-value stops: Set stops based on the total dollar value of the spread position moving against you. If you've determined your maximum acceptable loss is $1,000, and the spread moves enough to generate that loss, exit the entire position regardless of what individual legs are doing.

Percentage-based stops: Consider using percentage-based stops relative to the spread value at entry. For example, you might exit if the spread moves 15% against your position from entry. This approach scales with the size and volatility of your position.

Volatility-adjusted stops: Account for normal spread volatility when setting stops. Stops set too tight will get triggered by routine fluctuations that don't represent a failed trade thesis. Analyze the average true range or standard deviation of the spread to determine appropriate stop distances. If the spread typically moves $10 per day in normal conditions, a $5 stop is likely too tight and will result in premature exits.

Technical stops: Place stops beyond key technical levels on the spread chart. If you enter a long crush position because the spread is bouncing off support, place your stop below that support level. This gives the trade room to work while defining a clear invalidation point for your thesis.

Individual leg monitoring: While your stop should focus on the overall spread value, monitor each leg individually for unusual price action, execution problems, or liquidity concerns. If one leg experiences extreme volatility or unusual trading patterns, this might warrant an early exit even if the spread hasn't hit your stop level.

Liquidity and execution risks in multi-leg spreads

Liquidity is a critical but often overlooked consideration when trading multi-leg spreads. While the individual soybean, meal, and oil contracts are generally liquid, executing all three legs simultaneously at favorable prices requires careful attention to market conditions and execution techniques.

Understanding leg risk

Leg risk refers to the possibility that you'll get filled on one or two legs of your spread but not all three, leaving you with unintended directional exposure. This is one of the most significant execution risks in spread trading.

Imagine you're trying to enter a long crush position during a volatile market session. You successfully buy soybean meal and soybean oil, but before your soybean sell order fills, soybeans gap higher on breaking news. You're now long meal and oil with no offsetting short soybean position, creating directional risk you never intended to take.

This scenario illustrates why execution order and timing matter enormously in spread trading. If you execute legs separately rather than simultaneously, you're exposed to leg risk during the time between fills. This risk is particularly acute during:

• Periods of high volatility when prices are moving quickly

• Economic data releases or USDA crop reports that affect grain markets

• Market opens or closes when liquidity transitions

• Low-volume periods when individual orders have a larger market impact

Spread order entry vs. individual legs

Traders have two primary options for executing spread trades:

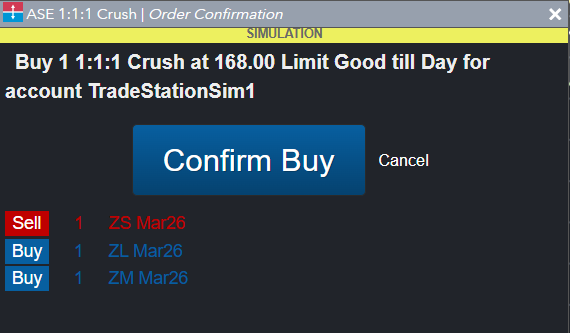

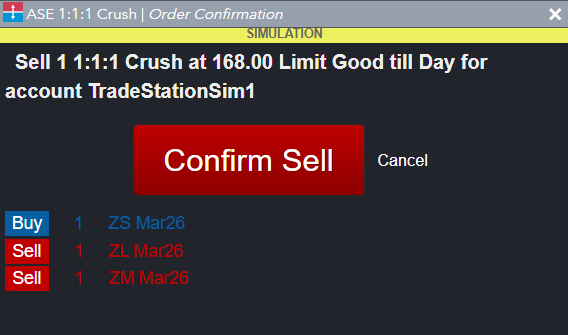

Spread orders (combination orders): TradeStation’s FuturesPlus allows you to submit all three legs as a single spread order. The entire order executes simultaneously (all legs filled together) or not at all, eliminating leg risk. This is the preferred method for most spread traders.

The trade-off is that spread orders may yield wider bid-ask spreads than working individual legs separately. The market maker that fills your spread order must manage the risk of assembling all three legs and charge for that service by widening spreads. However, this cost is typically worth it for the risk-reduction benefits.

Individual leg execution: Some experienced traders choose to work individual legs separately, either to achieve better execution prices or to scale into positions gradually. This approach requires careful timing and market monitoring to avoid leg risk.

If you choose this method, follow these guidelines:

• Execute during liquid market hours when all contracts are actively trading

• Use limit orders rather than market orders to control fill prices

• Monitor the spread value in real-time and be prepared to cancel if conditions change

• Have a plan for what to do if you get partially filled (immediately flatten the filled legs or aggressively work the remaining legs)

Market hours and liquidity Considerations

All three contracts in the crush spread (soybeans, soybean meal, and soybean oil) trade during both regular pit hours and electronic sessions. However, liquidity varies significantly across different time periods:

Regular trading hours: The highest liquidity occurs during regular CBOT trading hours when both electronic and pit trading overlap. This is generally the best time to execute complex spreads, as you'll encounter tighter bid-ask spreads, deeper markets, and more competitive pricing.

Electronic-only hours: During overnight and early morning electronic sessions, liquidity is typically lower. While you can still execute spreads during these periods, you may encounter wider bid-ask spreads and more slippage, particularly on the soybean oil contract, which tends to be the least liquid of the three.

Major report releases: Be particularly cautious around USDA crop reports, export sales data, and other scheduled releases that significantly impact grain markets. Volatility spikes during these periods, and liquidity often dries up immediately before the release as market makers pull back. If you must enter or exit during these periods, use spread orders to manage leg risk.

Slippage and market impact

Slippage refers to the difference between the price you expected to receive and the price you actually get filled at. In spread trading, slippage can occur on multiple levels:

Position size impact: The larger your position size, the more susceptible you are to slippage. While a single board crush (30 contracts total) might execute with minimal slippage during liquid hours, a position of 5 or 10 board crushes could move the market as it fills, particularly in the less liquid soybean oil contract.

Contract liquidity differences: Soybeans typically have the deepest liquidity, followed by soybean meal, with soybean oil generally being the least liquid. This means your soybean oil leg is most likely to experience slippage, especially during lower-volume periods. When sizing positions, consider the liquidity of your least liquid leg.

Bid-ask spread costs: Even with simultaneous execution, you'll typically pay the bid-ask spread on each leg. For a three-leg spread, these costs add up. Calculate the total bid-ask spread cost before entering trades, and ensure your expected profit justifies these transaction costs.

Exit slippage: Slippage often increases when exiting positions, particularly if you need to exit quickly due to a stop loss or adverse news. Factor this into your risk calculations. If you expect 2 ticks of slippage on entry and potentially 3-4 ticks on a rushed exit, your actual risk is higher than the nominal stop distance suggests.

Using TradeStation FuturesPlus for crush spread trading

Because crush spreads involve multiple legs and contract ratios, having the right platform tools is essential. TradeStation's FuturesPlus platform provides comprehensive tools for analyzing and trading complex spreads, such as the soybean crush. Understanding how to use these features effectively can significantly improve your ability to identify, execute, and manage spread positions.

Accessing the board crush spread

FuturesPlus makes it easy to access the properly weighted board crush spread. Simply type 'crush' or 'ZM' into the Instruments search to select the board crush. This automatically configures the 10:11:9 ratio (10 soybeans, 11 soybean meal, 9 soybean oil) that accurately reflects the processing relationship.

Once selected, you can open MD Traders (market depth), Order Tickets, charts for analysis, and other tools using this default configuration. This eliminates the need to manually calculate contract ratios or remember the proper weighting.

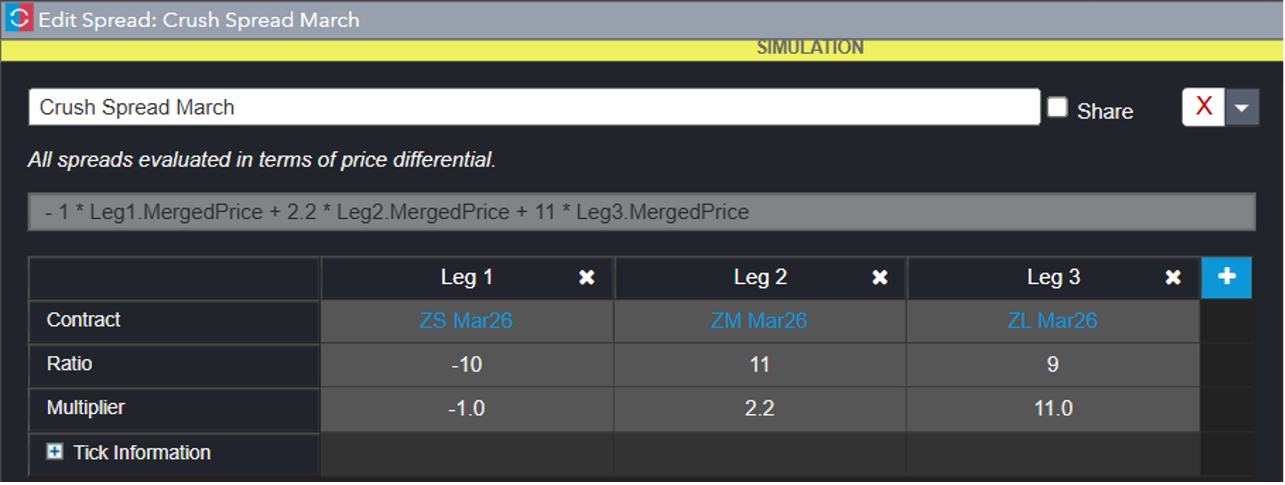

Customizing spreads with Autospreader®

For traders who want more control over their spread configurations, FuturesPlus offers Autospreader®, which allows you to configure custom spreads for analyzing and trading. When creating a crush spread in Autospreader®:

• Specify the contract month you want to trade

• Enter the correct ratios and multipliers, which adjust for contract size differences:

◦ Soybeans (ZS): ratio -10 with a -1 multiplier

◦ Soybean Meal (ZM): ratio 11 with a 2.2 multiplier

◦ Soybean Oil (ZL): ratio 9 with an 11.0 multiplier

Once you've named and saved your custom spread, you can select it to create the widgets needed for analysis and trading. An advantage of Autospreader® is that you can instantly open multiple MD Traders, Market Grids, and charts, with the spread and individual legs shown in separate tabs or windows for comprehensive monitoring.

Spread analysis tools

FuturesPlus provides several powerful tools for analyzing crush spreads:

Spread charting: The platform displays the spread value as a single instrument on price charts, making it easier to identify trading opportunities, support and resistance levels, and trend patterns. You can apply technical indicators directly to the spread chart rather than trying to calculate spread values manually.

Technical indicators: Apply customizable technical indicators (moving averages, RSI, MACD, Bollinger Bands, and more) directly to spread charts. This allows you to identify overbought or oversold conditions, momentum shifts, or potential reversal points in the spread relationship.

Order entry and execution

FuturesPlus streamlines the process of entering and managing multi-leg spread orders:

Multi-leg spread orders: Submit all three legs as a single spread order, reducing leg risk by ensuring all components execute simultaneously or not at all. The platform handles the complexity of routing and managing the individual leg orders.

Quick order adjustments: FuturesPlus provides features to quickly scale in or out of positions, adjust stop levels, or modify profit targets without canceling and re-entering complex multi-leg orders.

Risk management features

The platform includes several risk management tools specifically useful for spread trading:

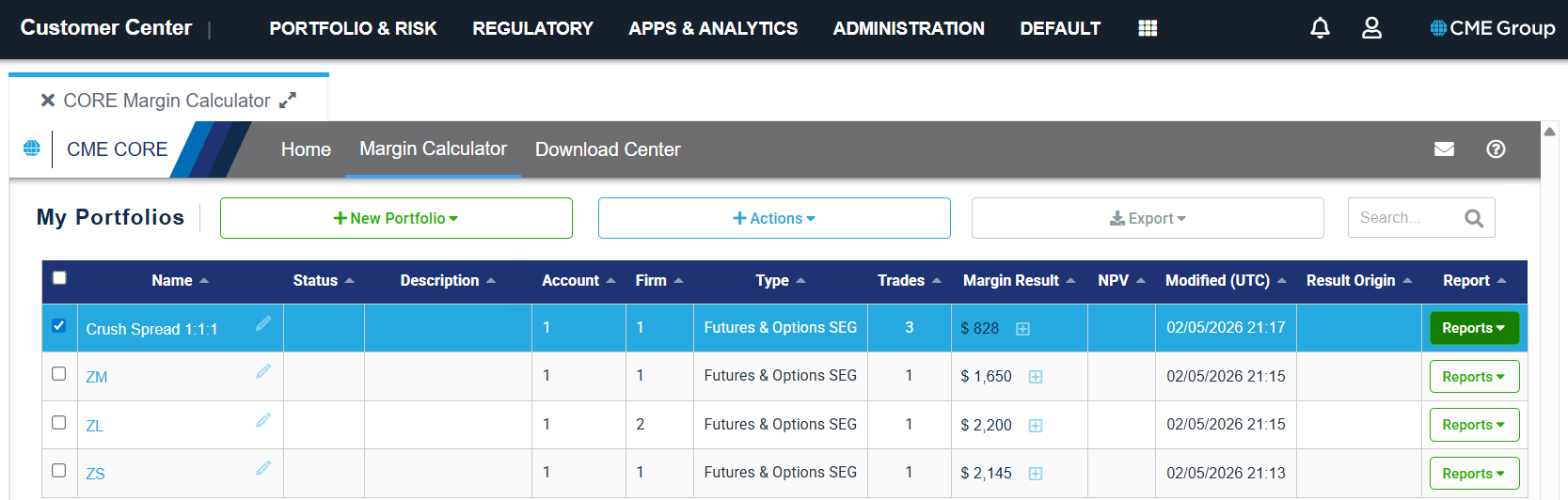

Real-time margin tracking: Monitor your margin usage across all positions in real-time. FuturesPlus clearly displays your available margin, margin requirements for current positions, and how much margin capacity you have for additional trades.

Position monitoring dashboard: View each leg's performance and the overall spread value in a unified dashboard. This makes it easy to monitor how the spread is performing and whether individual legs are behaving as expected.

Automated alerts: Set up automated alerts to notify you when spreads reach predetermined levels, when margin requirements change, or when specific market conditions occur. These alerts help you stay on top of positions even when you're not actively watching the market.

Simulated trading mode: Practice before you risk capital

Perhaps the most valuable feature for traders learning spread strategies is FuturesPlus' simulated trading mode. This environment allows you to practice crush spread strategies using real market data without risking real capital.

The simulation environment replicates live trading conditions as closely as possible, helping you:

• Understand the mechanics of placing spread orders and managing multi-leg positions

• Test your entry and exit strategies to see how they perform in real market conditions

• Gain confidence in your ability to execute complex trades before committing real money

• Learn how the platform's tools and features work without financial consequences for mistakes

• Experience the psychological aspects of managing positions through adverse market moves

You should practice any spread-trading strategy extensively in simulated trading before committing real capital. Only when you've demonstrated consistent proficiency in the simulated environment should you consider transitioning to live trading, and even then, start with minimal position sizes as you build real-world experience.

Essential risk disclosures

Before implementing any crush spread strategy, it's essential to fully understand the risks inherent in futures spread trading:

Substantial risk of loss: Futures trading involves substantial risk of loss, including the possibility of losing more than your initial investment, and is not suitable for all investors. You can lose more than your initial investment, especially with leveraged positions. The reduced margins typical of spread trading do not reduce the potential for significant losses if the spread moves substantially against your position.

Correlation risk: While spread trading may offer reduced volatility compared to outright positions, the relationships between soybeans, meal, and oil can and do change unexpectedly due to weather, government policies, global economic conditions, and countless other factors. These relationships can break down in ways that generate significant losses, even though the positions are structured as hedges between related products.

Historical patterns don't guarantee future results: No historical pattern or spread relationship is guaranteed to repeat. Seasonal tendencies, mean reversion expectations, and historical ranges provide context but never certainty. Market conditions change, and strategies that worked in the past may not work in the future.

Leverage magnifies losses: The low margin requirements in spread trading create temptation to overleverage. While a small margin requirement means you can control a larger position with less capital, losses are magnified proportionally. A seemingly small adverse move in the spread can wipe out a significant portion of your account if you're overleveraged.

Execution and liquidity risks: Multi-leg spreads carry execution risks that don't exist with single-contract positions. Leg risk, slippage, wider bid-ask spreads during volatile periods, and liquidity differences across contracts can all affect your actual results relative to your planned strategy.

Margin call risk: Even though spread positions may start with lower margins, exchanges can increase margin requirements during periods of volatility. You must maintain adequate capital reserves to meet potential margin calls, or you risk having your positions liquidated at the worst possible time.

Only risk capital you can afford to lose: Only trade with risk capital – money you can afford to lose without affecting your financial stability or lifestyle. Futures trading should never involve funds needed for living expenses, retirement, education, or other essential purposes.

These disclosures are not intended to discourage trading but to ensure that traders fully understand the risks before committing capital.

Conclusion: Approaching crush spreads with discipline

The soybean crush spread offers traders an opportunity to participate in grain-processing markets with potentially lower volatility and margin requirements than outright positions. By trading the relationship between soybeans and their processed products, crush spreads allow you to focus on processing economics without taking directional views on the absolute price of soybeans.

However, these benefits come with unique risks. Correlation breakdown, execution challenges, complex margin dynamics, and the ever-present danger of overleveraging all require careful attention and disciplined risk management. Long-term success with crush spreads demands:

• Thorough understanding of how the spread works and what drives it

• Disciplined position sizing that accounts for your true risk tolerance

• Systematic entry and exit strategies defined before entering trades

• Careful attention to execution quality and liquidity conditions

• Mastery of the tools available through TradeStation FuturesPlus

• Extensive practice in simulated trading before risking real capital

TradeStation's FuturesPlus platform provides the comprehensive tools you need to analyze, execute, and manage crush spread positions effectively. From built-in spread charting and historical analysis to multi-leg order entry and real-time risk monitoring, the platform streamlines what would otherwise be a complex and error-prone process.

Most importantly, take full advantage of FuturesPlus' simulated trading mode. Use it to practice until you can consistently demonstrate proficiency in identifying opportunities, executing trades, managing positions, and handling adverse scenarios. The simulation environment offers a risk-free way to develop the skills and confidence necessary for live trading.

When you do transition to live trading, start small. Use small position sizes initially, regardless of your margin. As you gain real-world experience and prove your strategy works in live markets, you can gradually scale up. Remember: professional traders built their success through disciplined risk management and continuous learning, not through aggressive position sizing and wishful thinking.

With disciplined preparation and consistent risk management, traders can approach crush spread strategies with greater confidence and clarity.

For more educational content on futures spreads and advanced trading strategies, visit TradeStation's Futures Education Center at www.tradestation.com. And remember always trade responsibly and within your risk tolerance.

Important Information and Disclosures

Futures trading is not suitable for all investors. To obtain a copy of the futures risk disclosure statement visit www.TradeStation.com/DisclosureFutures.

Margin trading involves risks, and it is important that you fully understand those risks before trading on margin. The Margin Disclosure Statement outlines many of those risks, including that you can lose more funds than you deposit in your margin account; your brokerage firm can force the sale of securities in your account; your brokerage firm can sell your securities without contacting you; and you are not entitled to an extension of time on a margin call. Review the Margin Disclosure Statement at www.TradeStation.com/DisclosureMargin.

Any examples or illustrations provided are hypothetical in nature and do not reflect results actually achieved and do not account for fees, expenses, or other important considerations. These types of examples are provided to illustrate mathematical principles and not meant to predict or project the performance of a specific investment or investment strategy. Accordingly, this information should not be relied upon when making an investment decision.

ID559590 D0526