Options Education Center

Crafting strategic straddles: turn earnings into opportunities

Crafting strategic straddles: turn earnings into opportunities Learn about straddles and how you can use this strategy effectively.

Download workspace

Scan for stocks on the move and identify opportunities to implement a straddle strategy.

DownloadExplore Strategies

Discover options strategies and empower your trading with the knowledge and skills to navigate dynamic market conditions.

Learn moreStraddle opportunities for earnings

A straddle is a multi-leg options strategy enabling investors to potentially profit from significant price fluctuations in a stock, typically associated with events like earnings announcements. This position can also benefit from heightened volatility realizing profits upon closing if the options are sold for a price higher than their initial purchase cost.

Five reasons straddles might be right for you

- Multi-directional strategy: Straddles can profit from both upward and downward price movements.

- Limited risk: The maximum loss is limited to the premium paid.

- Lower cost: Straddles require less capital compared to buying or shorting stock.

- Reduced need for accuracy in price forecast: Straddles benefit from a significant price movement before expiration, without the need for exact predictions.

- Potential profit: Profits can potentially be unlimited if the price moves favorably before expiration.

Things to watch for when trading straddles

Additional premiums

Both the call and put options require premiums to be paid.Substantial price movement necessary

Profiting from a straddle requires a sizable price change in the underlying asset.Efficient markets

The market often factors in potential movements, making it challenging to profit from a straddle.Trade management required

Active position management is crucial for risk and profit control. Depending on market conditions, selling the straddle may be necessary to capture gains or limit losses.Additional premiums

Both the call and put options require premiums to be paid.Substantial price movement necessary

Profiting from a straddle requires a sizable price change in the underlying asset.Efficient markets

The market often factors in potential movements, making it challenging to profit from a straddle.Trade management required

Active position management is crucial for risk and profit control. Depending on market conditions, selling the straddle may be necessary to capture gains or limit losses.Quick reference guide: Long straddle | |

|---|---|

Market outlook | Anticipating a sharp price move in either direction and/or increased volatility |

Position net debit or credit | Debit (premium paid) |

Number of legs | Two – one long call and one long put with identical strikes and expirations |

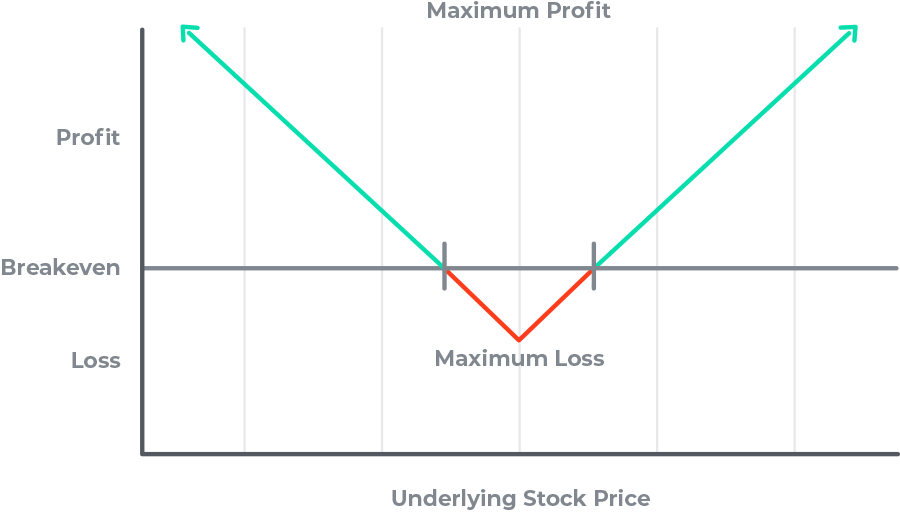

Maximum profit | Unlimited upward, or from the strike price to zero downward |

Profits from | Underlying price moving significantly in either direction rapidly |

Maximum loss | Premium paid to enter the position, occurs if both options expire worthless |

Breakeven | There are two, the strike minus the premium paid and the strike plus the premium paid |

Risk from | Underlying price not moving sufficiently to cover the cost of the position and/or a decline in volatility |

Options level required | Level 3 – Click here for additional information |

What is a straddle?

A straddle is a multi-leg debit spread that involves two key actions.

Buy a call option

This leg captures upside/bullish profit potential. It benefits from a rise in the underlying price or an increase in volatility. The strike price should closely align with the current underlying price.Buy a put option

Simultaneously, buy a put option with the same strike and expiration as the call. This leg profits from a drop in the underlying price or an increase in volatility.The straddle risk/reward profile

Reward

Realized when both options are sold. Profit equals the sale price of both options minus the premium paid at purchase. This can happen if the underlying price moves significantly or if implied volatility rises.

Breakeven

There are two breakeven points – the strike plus the premium paid, and the strike minus the premium paid.

Risk

The amount paid for both options. The loss would be realized if both options expire with the underlying trading at the strike price.

Situations suited for a straddle

Common situations where a straddle may be used include:

Traders might opt for a straddle when anticipating a substantial, rapid price movement in the underlying, or, when the current implied volatility is low and expected to increase rapidly.

Three to four weeks before an earnings announcement

Approximately one month before an earnings announcement, implied volatility is often low compared to the week of the report. Options can be inexpensive during this period of low-volatility. As the earnings date approaches, the uncertainty of the number increases volatility. The positive Vega of long options also causes the options’ value to rise. Avoid entering the straddle in the days before the earnings report is released, as purchasing the straddle during such periods of elevated volatility would lead to overpayment. After earnings are released, volatility typically decreases, and the Vega of the straddle will drop the value of the options. This decline might even surpass the profit gained from Delta and price movement.

Limited risk

Expecting a significant price move but uncertain about the direction.

A drastic increase in volatility

If the current implied volatility is very low but it is expected to increase soon. Typically, volatility is low or dropping while the price of an underlying is gradually rising. If the price turns down at a resistance level or the trend becomes bearish, the volatility will usually rise.

How to place a straddle trade

<Embed Code for Long Straddle Options Strategies/>

- Select a stock

Identify a stock with an earnings announcement in three to four weeks. - Check implied volatility (IV)

Compare current IV to the past year. Historically it should be relatively low, with the stock demonstrating a pattern of elevated volatility leading up to earnings announcements. - Choose strike prices and expiration

Select a call and a put option near the current underlying price. Choose an expiration of more than 30 days after the announcement to mitigate extreme time decay. Both options should share the same expiration date. - Risk management

The combined premium paid is the maximum risk. Two breakeven points exist: - Upward breakeven. The strike plus premium paid.

- Downward breakeven. The strike minus premium paid.

- Analysis

Examine historical earnings price movements to ensure that the average movement surpasses the necessary price shift needed to exceed the breakeven points. Additionally, assess the prior implied volatility movement to determine if there is a significant increase in IV, potentially benefiting from Vega for profit. - Vega is the premium movement for every 1 percent change in volatility.

- Imagine an option premium is $16, the Vega is 0.31, and IV is 47.69%. If the IV moves up to 48.69% then the new premium would be $16.31 assuming nothing else changes.

Exiting the straddle

- Exit the spread by simultaneously selling both the call and the put. A profit is realized if both are sold at a higher combined price than the premium paid at the opening. The profit is the premium collected from selling the straddle minus the opening cost, excluding commissions and fees.

- One of the options will appreciate in value while the other depreciates. Both options are sold to recoup the time value left.

- Consider exiting early if the IV significantly increases before the earnings announcement, as Vega will boost options values.

Still unsure? Sharpen your straddle skills with simulated trading

Access the TradeStation platform in Simulated Trading mode to familiarize yourself with the strategy and order execution. Practice placing the spread in a risk-free environment until you feel confident.

ID3296067D0124

Conclusion

A straddle, which involves the purchase of a call and a put with the same strike and expiration, is a valuable strategy for traders seeking to profit from significant price movements during events like earnings releases. This approach can capitalize on both substantial price shifts and an increase in implied volatility, boosting the value of the purchased options.

ID3296067 D0124